Introduction

Life is unpredictable. Unexpected events such as job loss, medical emergencies, vehicle repairs, or home maintenance costs can create significant financial pressure.

Without savings, many people rely on credit cards or loans to cover these expenses, which can lead to debt and financial stress.

An emergency fund acts as a financial safety net that helps protect you during difficult situations.

Building an emergency fund is often one of the first and most important steps in creating a strong financial foundation.

If you are new to money management, start with our What Is Personal Finance? guide.

What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected expenses or financial emergencies.

The purpose of an emergency fund is to provide financial protection when unforeseen situations occur.

Examples include:

• Job loss

• Medical emergencies

• Car repairs

• Home repairs

• Family emergencies

• Unexpected travel expenses

Emergency funds should only be used for genuine emergencies, not for discretionary purchases or entertainment.

According to the Consumer Financial Protection Bureau, emergency savings can improve financial resilience and reduce dependence on debt during difficult situations.

Why an Emergency Fund Is Important

Many people underestimate the financial impact of unexpected events.

Even a relatively small emergency can create significant stress if there are no savings available.

Financial Security

Emergency funds provide protection against unexpected expenses.

Reduced Stress

Knowing you have financial reserves can provide peace of mind.

Less Dependence on Debt

Savings reduce the need to use credit cards or loans.

Greater Financial Flexibility

Emergency savings provide options during difficult periods.

Better Long Term Financial Health

Avoiding unnecessary debt supports long term wealth building.

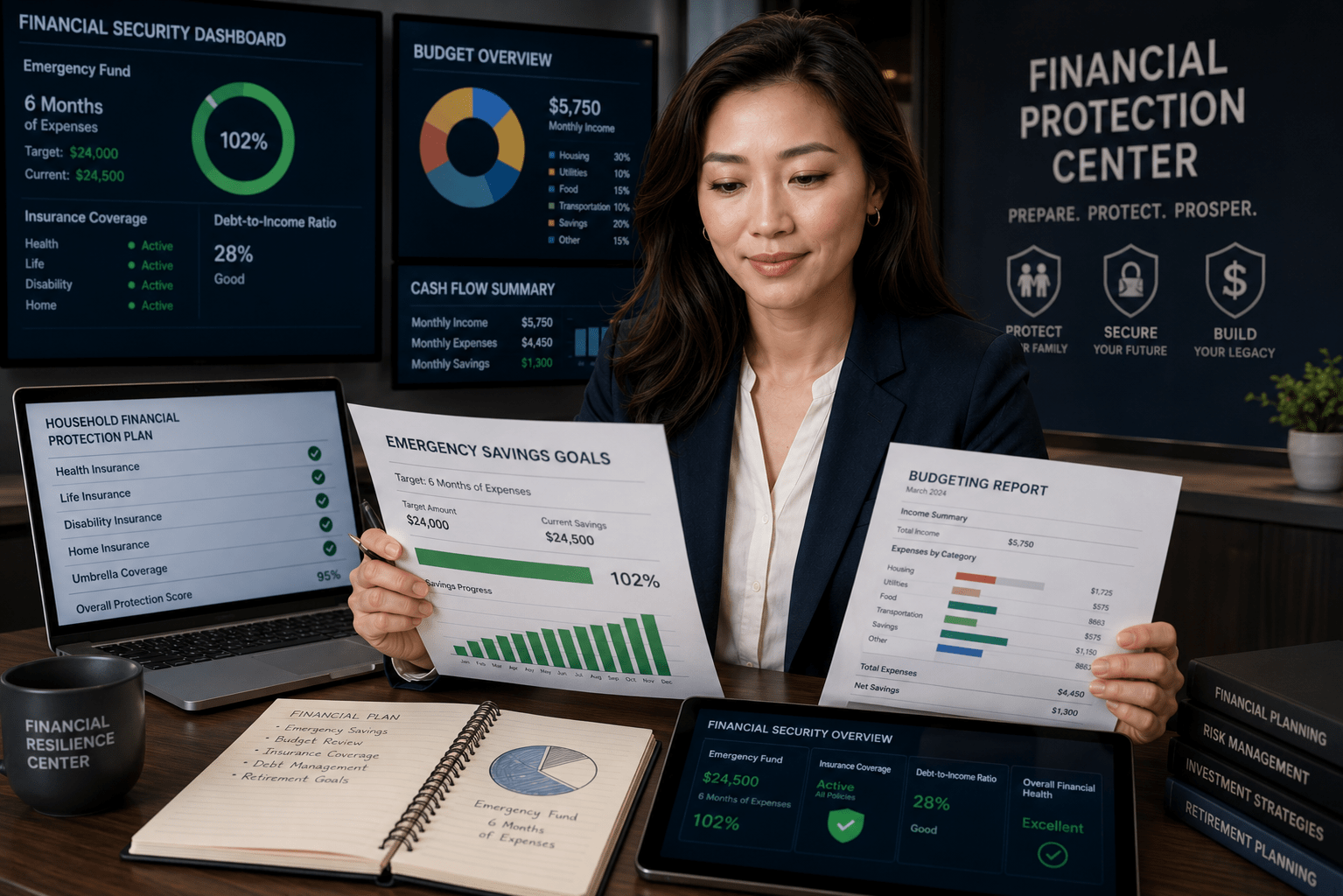

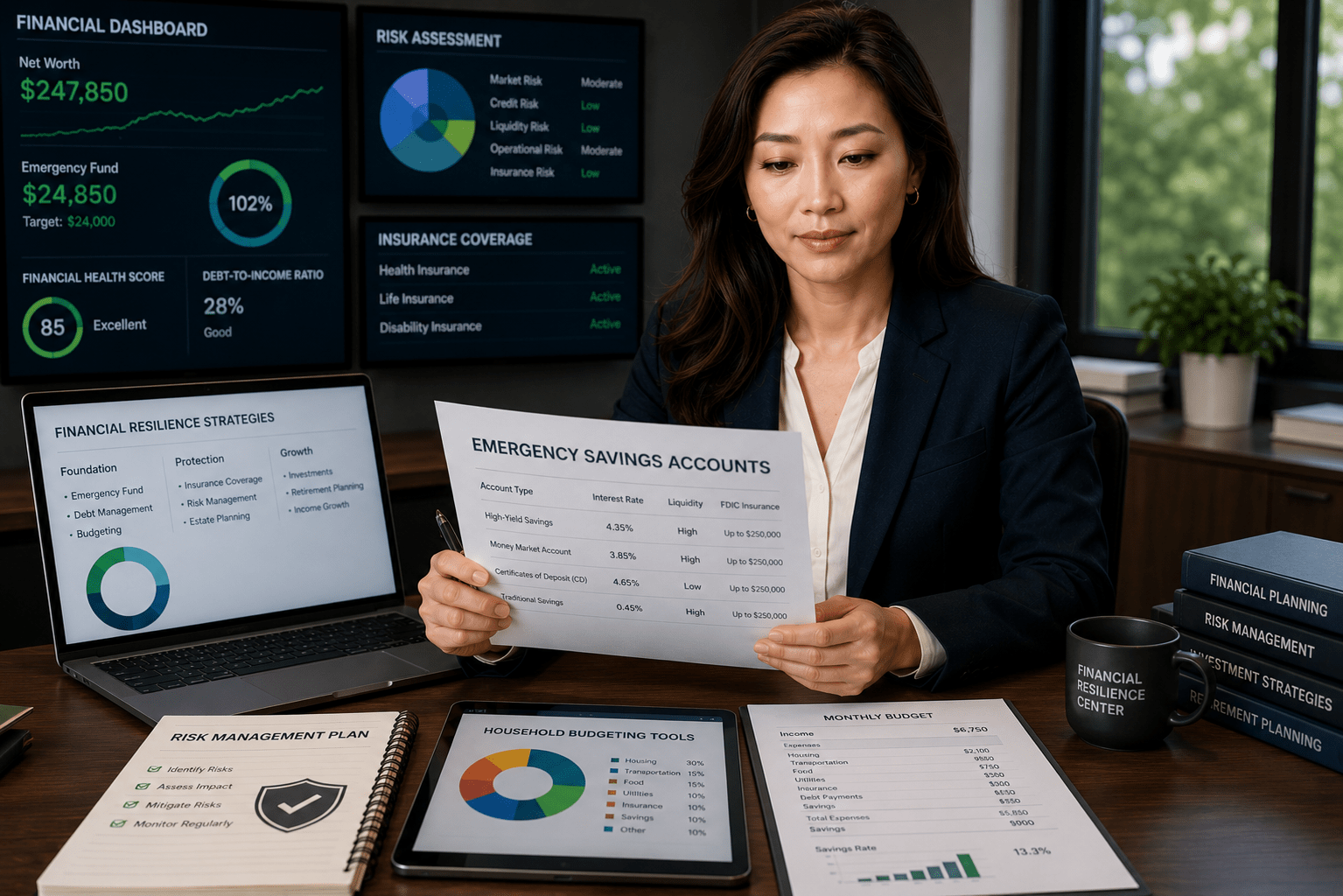

How Much Should You Save in an Emergency Fund?

The ideal emergency fund depends on individual circumstances.

However, most financial experts recommend saving between three and six months of essential living expenses.

Three Months of Expenses

Suitable for individuals with:

• Stable employment

• Multiple income sources

• Strong job security

Six Months of Expenses

Often recommended for:

• Self employed individuals

• Business owners

• Freelancers

• Households with variable income

More Than Six Months

Some people choose to save additional reserves if:

• Their industry is unstable

• They support dependents

• Their income fluctuates significantly

What Expenses Should Be Included?

When calculating emergency fund targets, focus on essential expenses.

Examples include:

• Housing costs

• Utilities

• Groceries

• Insurance

• Transportation

• Healthcare

• Debt obligations

Discretionary spending is generally not included.

Where Should You Keep an Emergency Fund?

Emergency savings should be:

• Easily accessible

• Secure

• Separate from everyday spending accounts

Common options include:

• High yield savings accounts

• Traditional savings accounts

• Money market accounts

The primary goal is safety and accessibility rather than maximizing investment returns.

Research from the Federal Reserve Consumer Resources highlights the importance of maintaining liquid savings for emergencies.

How to Build an Emergency Fund

Many people feel overwhelmed by large savings targets.

The good news is that emergency funds can be built gradually.

Step 1: Set a Realistic Goal

Start with an achievable target.

Examples:

• $500

• $1,000

• One month of expenses

Small goals create momentum.

Step 2: Create a Budget

A budget helps identify opportunities to save consistently.

Readers who have not yet created a budget should review our How to Create a Personal Budget guide.

Step 3: Automate Savings

Automatic transfers help build savings without requiring constant effort.

Even small amounts can grow significantly over time.

Step 4: Reduce Unnecessary Spending

Review discretionary expenses and identify areas for improvement.

Examples include:

• Unused subscriptions

• Frequent dining out

• Impulse purchases

• Non essential upgrades

Step 5: Increase Income

Additional income sources can accelerate emergency fund growth.

Examples include:

• Freelancing

• Side businesses

• Part time work

• Selling unused items

Common Emergency Fund Mistakes

Keeping Too Little

Insufficient savings may not provide meaningful protection.

Using the Fund for Non Emergencies

Emergency funds should only be used when necessary.

Investing Emergency Savings

Emergency funds should remain accessible and low risk.

Stopping After Reaching a Small Goal

Continue building toward long term targets.

Ignoring Inflation

Review savings goals periodically and adjust when necessary.

Emergency Fund vs Investing

Many beginners wonder whether they should save or invest first.

In most situations:

- Build an emergency fund first.

- Then focus on investing.

Emergency savings provide protection that investments cannot guarantee in the short term.

Readers interested in growing wealth should explore our upcoming Investing for Beginners guide.

Benefits of Having an Emergency Fund

Better Financial Confidence

You know you can handle unexpected situations.

Improved Financial Stability

Emergency savings create a stronger financial foundation.

Reduced Reliance on Credit

Less borrowing means lower interest costs.

Greater Peace of Mind

Financial preparedness reduces uncertainty.

Stronger Long Term Financial Progress

Unexpected expenses are less likely to derail financial goals.

Frequently Asked Questions

What is an emergency fund?

An emergency fund is money saved specifically for unexpected expenses and financial emergencies.

How much should I save?

Most financial experts recommend three to six months of essential living expenses.

Where should I keep emergency savings?

A secure and easily accessible savings account is usually the best option.

Can I invest my emergency fund?

Emergency funds should generally remain in low risk and easily accessible accounts.

Personal Finance Disclaimer

This article is for educational purposes only and should not be considered financial, investment, tax, or legal advice. Consult qualified professionals before making important financial decisions.

Conclusion

An emergency fund is one of the most important components of personal finance.

By creating dedicated emergency savings, individuals can improve financial security, reduce stress, and protect themselves from unexpected financial challenges.

Building an emergency fund takes time, but even small consistent contributions can create meaningful protection and support long term financial success.