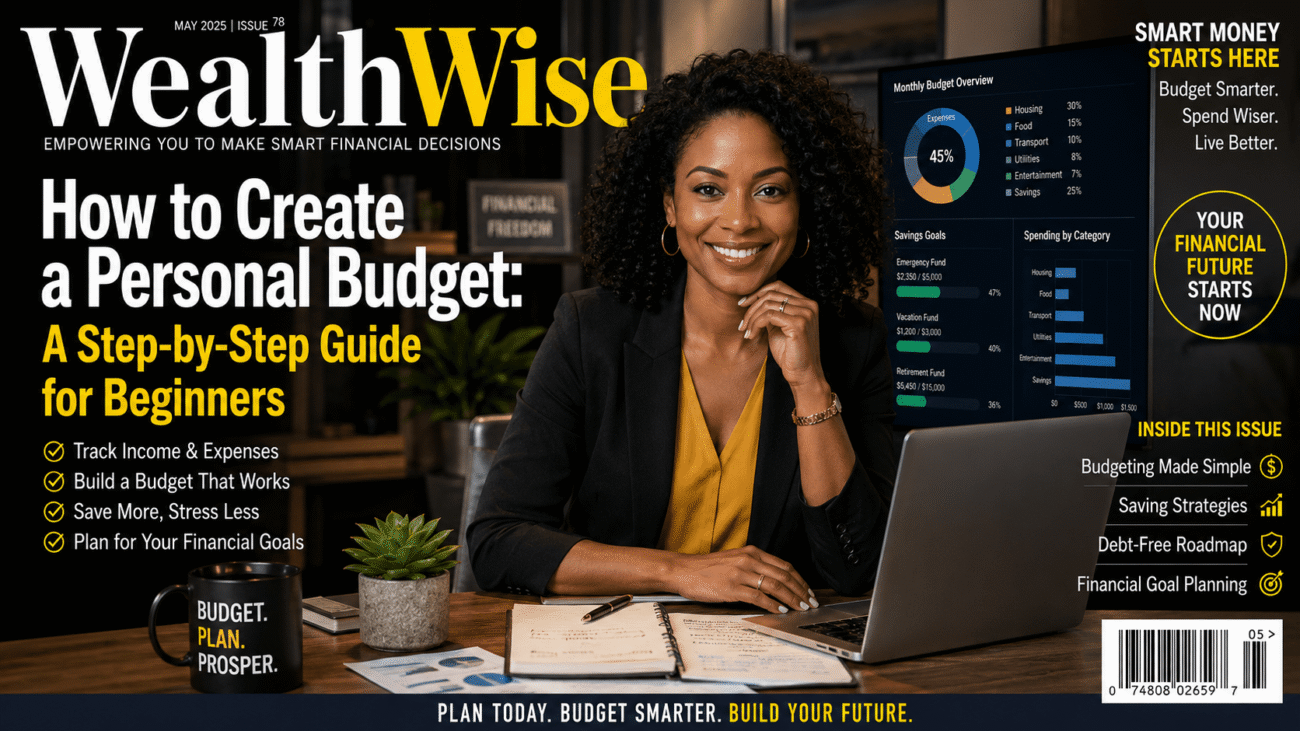

Introduction

Creating a budget is one of the most important steps you can take to improve your financial health.

A personal budget helps you understand where your money comes from, where it goes, and how much you can save for future goals.

Without a budget, it is easy to overspend, accumulate debt, and lose track of financial priorities.

The good news is that budgeting does not need to be complicated. With a simple plan and consistent habits, anyone can take control of their finances.

If you are new to money management, start with our What Is Personal Finance? guide.

What Is a Personal Budget?

A personal budget is a financial plan that tracks income and expenses over a specific period, usually monthly.

It helps individuals:

• Control spending

• Increase savings

• Reduce debt

• Achieve financial goals

• Improve financial awareness

Budgeting provides a clear picture of your financial situation and helps you make informed decisions.

According to the Consumer Financial Protection Bureau, budgeting is one of the most effective ways to manage money and improve financial well being.

Why Budgeting Is Important

Many people believe budgeting limits freedom.

In reality, budgeting gives you more control over your money.

Benefits include:

Better Spending Control

You understand exactly where your money goes.

Increased Savings

Budgeting helps prioritize savings goals.

Reduced Financial Stress

A clear financial plan reduces uncertainty.

Faster Goal Achievement

Budgets help you allocate money toward important objectives.

Better Debt Management

Tracking expenses helps identify opportunities to pay off debt faster.

Step 1: Calculate Your Monthly Income

The first step in creating a budget is understanding how much money you earn.

Include all income sources such as:

• Salary

• Freelance work

• Business income

• Rental income

• Investment income

Use your average monthly income if earnings vary.

Step 2: Track Your Expenses

Next, identify where your money is going.

Review bank statements, receipts, and financial records.

Common expense categories include:

Housing

Rent or mortgage payments.

Transportation

Fuel, public transport, and vehicle expenses.

Food

Groceries and dining expenses.

Utilities

Electricity, internet, water, and phone bills.

Entertainment

Streaming services, hobbies, and leisure activities.

Savings and Investments

Money allocated toward future goals.

Tracking expenses often reveals spending habits that can be improved.

Step 3: Choose a Budgeting Method

Several budgeting methods can be effective.

The best approach depends on your goals and lifestyle.

The 50/30/20 Budget Rule

One of the most popular budgeting frameworks is:

• 50% Needs

• 30% Wants

• 20% Savings and Debt Repayment

The concept is illustrated below:

While this widget demonstrates how savings can grow through compounding, budgeting helps create the surplus needed to invest consistently.

The 50/30/20 budgeting rule is widely used because it is simple and flexible.

Zero Based Budgeting

In this method, every dollar of income is assigned a purpose.

Income minus expenses equals zero.

This does not mean spending everything. It means assigning all money to specific categories.

Pay Yourself First

This strategy prioritizes savings before spending on non essential items.

Many financial experts recommend automating savings immediately after receiving income.

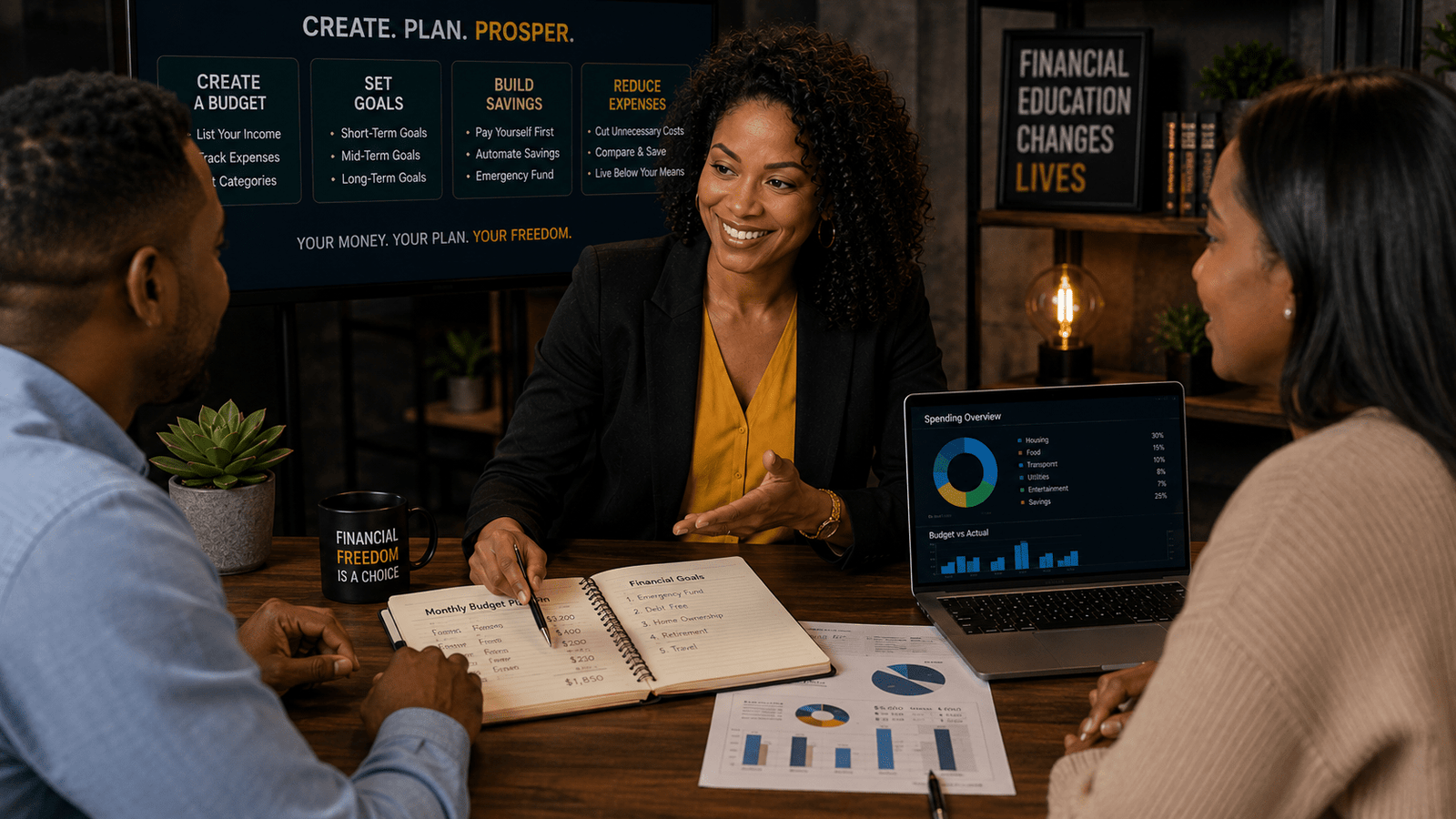

Step 4: Set Financial Goals

A budget works best when connected to specific goals.

Examples include:

Short Term Goals

• Vacation savings

• Paying off credit cards

Long Term Goals

• Buying a home

• Retirement planning

Readers interested in long term planning should revisit our Personal Finance Complete Guide.

Step 5: Reduce Unnecessary Spending

After reviewing expenses, identify areas where spending can be reduced.

Common opportunities include:

• Unused subscriptions

• Frequent dining out

• Impulse purchases

• Excessive entertainment spending

Small changes often produce meaningful results over time.

Common Budgeting Mistakes

Setting Unrealistic Goals

Budgets should be practical and sustainable.

Forgetting Irregular Expenses

Include annual or seasonal costs.

Not Tracking Spending

Monitoring progress is essential.

Giving Up Too Quickly

Budgeting improves with practice.

Ignoring Savings

Always include savings as part of your budget.

Budgeting Tips for Success

• Review your budget monthly

• Automate savings

• Track expenses regularly

• Adjust when circumstances change

• Focus on long term consistency

Successful budgeting is not about perfection. It is about making informed decisions consistently.

Research from the Federal Reserve Consumer Resources highlights the importance of planning, saving, and financial preparedness.

Frequently Asked Questions

What is the best budgeting method?

The best method depends on personal preferences, but the 50/30/20 rule is popular for beginners.

How often should I review my budget?

Most people should review their budget monthly.

Can budgeting help reduce debt?

Yes. Budgeting helps identify extra funds that can be directed toward debt repayment.

Is budgeting difficult?

No. Modern budgeting apps and simple spreadsheets make budgeting easier than ever.

Personal Finance Disclaimer

This article is for educational purposes only and should not be considered financial, investment, tax, or legal advice. Consult qualified professionals before making important financial decisions.

Conclusion

Creating a personal budget is one of the most effective ways to improve financial health.

By understanding income, tracking expenses, choosing a budgeting method, setting goals, and monitoring progress, individuals can gain greater control over their finances and build a stronger financial future.